The Venture Capital paradigm of “hitting a few winners and many misses” is wrong. Top-quartile US Venture Capital firms have outperformed the NASDAQ by ~2x in IRR since 2007.

The traditional Venture Capital investment paradigm relies on The Power Law. It assumes a handful of winners generate the bulk of the returns. That paradigm, coupled with the operational friction associated with sourcing, evaluating, and managing private-market deals, incentivizes VCs to build more concentrated portfolios.

Venture capital is hard. Unlike in the public markets, where investors can pick any company to invest in whenever they want, and all the data is available. In the private market VCs need to:

Building and managing a venture portfolio is extremely time consuming, which in turn leads VCs to create highly concentrated portfolios. The Power Law paradigm is a result of that reality.

However, the data is clear: companies are staying private longer, averaging ~14 years from inception to IPO vs. ~4 years during the early 2000s, while generating the majority of their appreciation in share price while private, driving the returns of the US venture asset class up into the right.

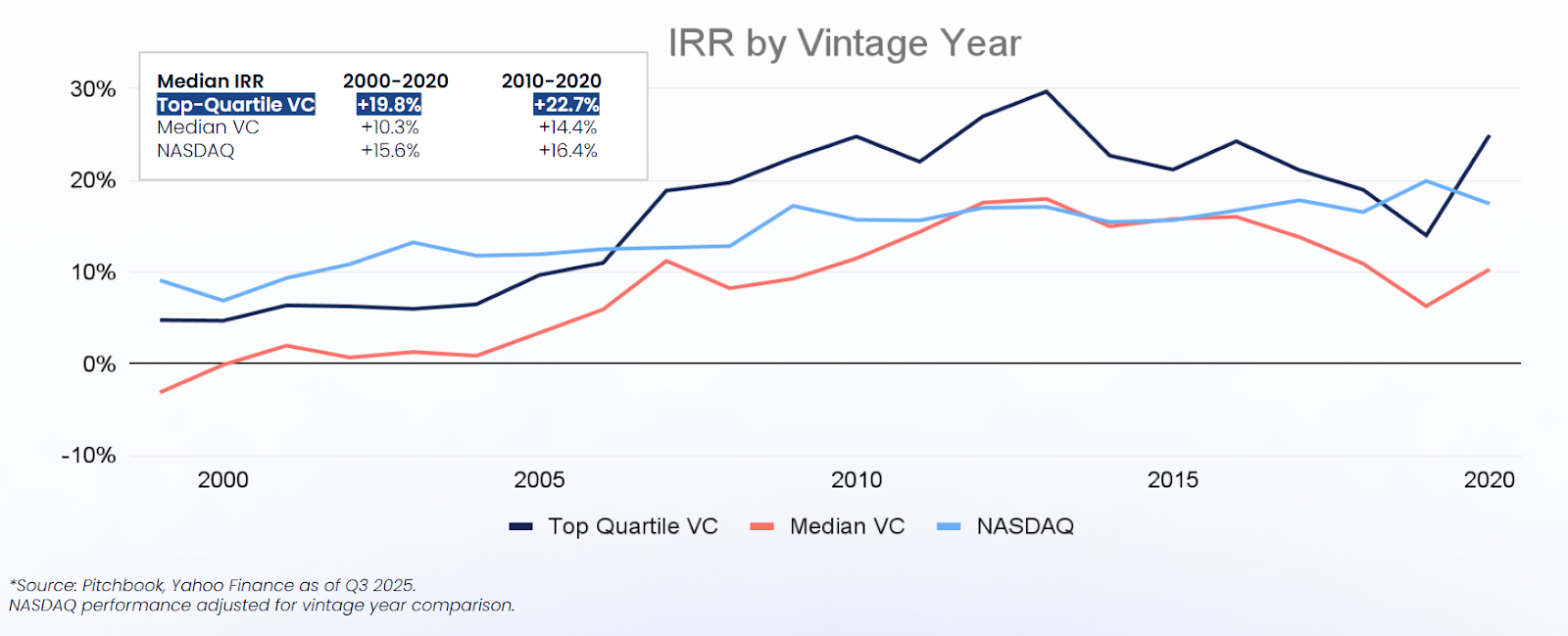

Specifically, from 2010 to 2020 the average IRR for the NASDAQ was 13.4% vs 27% for top quartile US VCs.

Outperforming the public markets is a well known challenge. Hence, the famous wager placed by Warren Buffet (arguably one of the best active investors to have ever lived) in 2007 says it all: he bet $1 million that a low-cost S&P 500 index fund would outperform a group of hedge funds over a 10-year period; and he won. The common truth is that the best investment from a risk-reward perspective is simply buying indexes such as the S&P 500 or the NASDAQ.

The data shows that this is also true for venture investments. Adding the fact the “top quartile Venture Fund” is a volatile definition. Having a fund at the top quartile doesn't guarantee that subsequent vintage funds will follow suit.

Thus, from a risk-reward perspective, investors are better off investing in an index that aims to mirror the performance of top quartile US VC managers. Since this theoretical index does not exist, we must look for a verifiable, diversified proxy that has overcome the friction associated with private investing at scale. Specifically, historical investments made through the Equitybee platform support this argument. Notably, more than 850+ funded companies within the Equitybee portfolio have generated a net realized IRR of ~28%+ while also outperforming top-decile US VCs in DPI across 6 of the last 7 vintage years. We could not identify a single US VC manager with such consistent returns; I would argue that this is the best proxy to indexing the late-stage US Venture / Growth market.

Equitybee provides investment access to almost any startup company with a significant discount at scale, by providing startup employees with the funding they need to exercise their stock options.

If you are still chasing unicorns, you might actually be betting more than investing. You are ignoring two decades of data.